8x8 Q1 FY2025 Earnings Deep Dive

In the first quarter of fiscal 2025 (period ended June 30, 2024), 8x8 reported total revenue of $178.1 million, a slight decline from $183.3 million in the same quarter of FY2024.

Financial Performance Overview (Q1 FY2025)

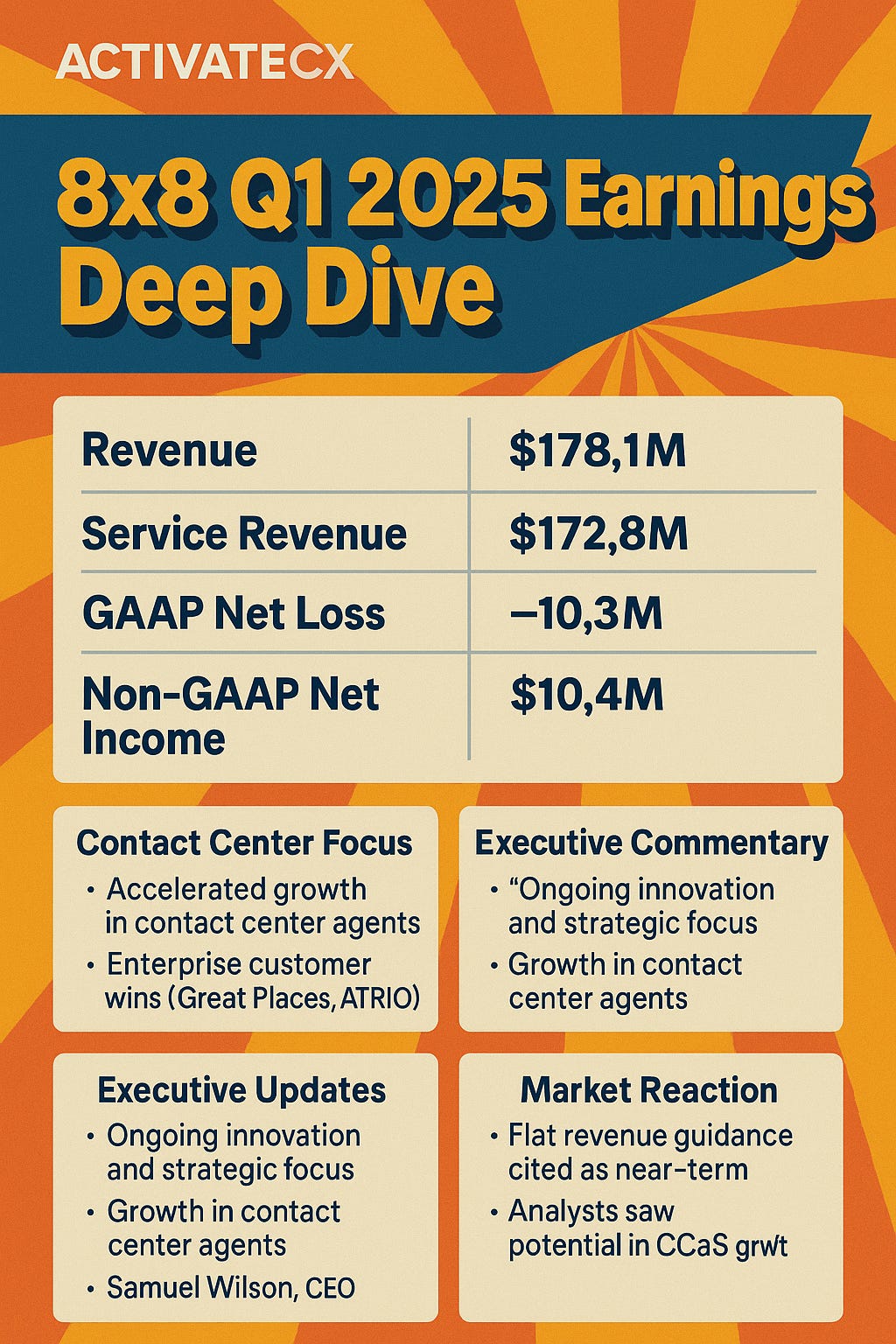

Revenue and Income: In the first quarter of fiscal 2025 (period ended June 30, 2024), 8x8 reported total revenue of $178.1 million, a slight decline from $183.3 million in the same quarter of FY2024. Service revenue (recurring subscriptions) was $172.8 million, down from $175.2 million a year ago. Despite the year-over-year drop (~3% lower revenue), sequential performance was stable – Q1 FY25 revenue was roughly flat compared to $179.4 million in Q4 FY2024. The company’s GAAP net loss narrowed to $10.3 million (improved from a $15.3 million loss in Q1 FY2024), reflecting cost controls and debt refinancing benefits. On a non-GAAP basis, 8x8 remained profitable: non-GAAP net income was $10.4 million for the quarter (versus $15.5 million in the prior year). Adjusted EBITDA came in at $25.8 million (down from $33.8 million in Q1 FY2024), and non-GAAP operating margin was about 11% – still within the company’s guidance range.

Growth Rates: Overall revenue fell ~2.8% year-over-year, attributable in part to the ongoing runoff of legacy revenues from 8x8’s 2022 Fuze acquisition. Management noted that excluding the decline in former Fuze platform customers, core service revenue would have grown nearly 5% YoY. Sequentially, total revenue was essentially flat (-0.7% vs. Q4), indicating that the business has stabilized on a quarter-to-quarter basis. Non-GAAP operating margin was around 11%, down from ~15% a year ago due to lower revenue and ongoing investments, but GAAP net loss improved versus last year as the company kept operating expenses in check.

Guidance: 8x8’s outlook at the time was cautious. For the next quarter (Q2 FY2025), management guided $175–$181 million in total revenue, implying roughly flat-to-slightly down YoY growth. Full-year FY2025 guidance was $710–$732 million in total revenue (approximately 0% to +0.5% growth over FY2024’s $729M) with a non-GAAP operating margin of 10–11%. This flat revenue forecast underscored the near-term growth challenges as 8x8 transitioned its customer base and product mix. Notably, the company announced it would discontinue reporting ARR (Annual Recurring Revenue) going forward, citing that an increasing portion of sales come from usage-based and CPaaS/communications API services which make the traditional ARR metric less relevant.

Segment Highlights: CCaaS Focus and Enterprise Activity

8x8 offers an integrated cloud platform (branded XCaaS™, or Experience Communications as a Service) that combines UCaaS (Unified Communications – voice, video, team chat) and CCaaS (Contact Center) capabilities on one platform. In Q1 FY25, the company emphasized the strong performance and strategic importance of its Contact Center-as-a-Service (CCaaS) segment:

Contact Center Growth: CEO Samuel Wilson noted “continued adoption of our modern CX platform” and accelerated growth in the number of contact center agents, especially among enterprise customers. This suggests that while overall revenue was flat-to-down, the CCaaS user base was expanding, indicating healthy demand for 8x8’s contact center solutions even as some legacy telephony (UCaaS) segments faced pressure. The win of new contact center seats helped offset churn in legacy products. Importantly, 8x8’s strategy of selling integrated UCaaS+CCaaS deals (XCaaS) to larger enterprises is resulting in larger deployments of contact center agents that drive higher-value subscriptions.

Enterprise Customer Wins: The quarter saw notable enterprise wins and expansions with an emphasis on contact center capabilities. For example, Great Places Housing Group (a UK housing provider with 25,000 homes) chose 8x8’s one-platform UCaaS & CCaaS solution, citing the platform’s reliability in the UK public sector and its omnichannel conversational AI, customer journey analytics, and reporting features tailored to their needs. In the US, ATRIO Health Plans selected 8x8’s integrated UCaaS and CCaaS (with 8x8 Voice for Microsoft Teams, Intelligent Customer Assistant, and Secure Pay) because 8x8 could meet stringent HIPAA-compliant contact center requirements (secure voice payments, compliant call recording storage) while providing future upgrade opportunities. These customer wins illustrate 8x8’s competitive positioning for organizations that require a combined communications and contact center platform with advanced compliance and AI capabilities.

Customer Retention and Churn: Management did acknowledge churn headwinds from the acquired Fuze customer base. Many former Fuze customers had not yet migrated to 8x8’s platform, resulting in year-over-year revenue attrition. This was evident in the 1% YoY decline in service revenue during the quarter, but excluding Fuze-related churn, service revenue was rising (~+5% YoY). The company is actively migrating remaining Fuze customers to 8x8 XCAAS and expects to complete all migrations by the end of calendar 2025. No specific large customer losses were cited in Q1, suggesting churn was mostly the known Fuze legacy accounts and some SMB attrition. The focus remains on improving customer retention and upselling the broader XCaaS platform to stabilize and grow recurring revenues.

Product & Platform Innovation Highlights

8x8’s Q1 FY25 was marked by significant product updates and new AI-powered capabilities across its platform, aimed at enhancing both the UCaaS and CCaaS offerings. Key operational highlights included:

AI Enhancements Across the Platform: 8x8 embedded new AI capabilities spanning its contact center and unified communications services. Notably, the company deployed a more powerful large-language model to improve speech transcription accuracy and expand language support for interaction analytics – provided to customers at no extra cost. They also introduced AI-based interaction summaries that integrate with CRM systems (e.g. Salesforce, Zoho), allowing contact center agents using the 8x8 Agent Workspace to quickly review summarized context from previous calls. Additionally, 8x8 enabled a “bring-your-own-AI” capability for its contact center – businesses can plug in their AI provider of choice (LLM) to generate call summarizations, which supervisors can access within the 8x8 workspace for valuable insights. On the unified communications side, 8x8 Meetings now offer AI-powered in-meeting “catch-up” summaries and post-meeting recap emails to facilitate follow-ups and action items. These AI features showcase 8x8’s push to infuse intelligence and automation into customer interactions and employee collaboration.

New Solutions Launches: The company launched several new services in Q1:

8x8 Ballot It! – an AI-powered self-service solution designed for UK local governments to boost voter engagement. Just ahead of the UK general elections, Ballot It! was released to give citizens quick access to election information (candidates, polling station details, required documents, etc.) via conversational AI, thereby encouraging higher voter turnout. This showcased 8x8’s ability to deliver purpose-built solutions using its contact center AI technology for civic use cases.

8x8 Intelligent Customer Assistant – Voice: Building on its chat-based virtual assistant, 8x8 added voice support to its Intelligent Customer Assistant. This voice conversational AI solution allows businesses to create natural, human-like self-service experiences over the phone. With multi-language support and regional customization, the voice bot can handle routine calls or tasks, seamlessly handing off to live agents when needed. Early adopter results were promising – for instance, Oldham Council in the UK implemented the 8x8 Intelligent Customer Assistant for voice and saved £40,000 annually while improving call handling success to over 80%, as agents could manage calls more efficiently alongside other tasks.

Interact for Proactive Outreach: 8x8 introduced a new omnichannel outbound messaging tool called Interact for Proactive Outreach. This enables organizations to communicate with customers at scale via SMS and WhatsApp, sending outbound messages (for reminders, marketing, notifications, etc.) and handling responses within the 8x8 contact center workflow. Inbound replies from those SMS/WhatsApp campaigns are automatically routed to agents or AI bots in the contact center. This feature was driven by customer demand – as companies recognize modern customer experience requires engaging on mobile messaging channels, not just calls or email.

Regal.io Partnership: In Q1, 8x8 announced that Regal.io (a cloud-based sales dialer platform) joined the 8x8 Technology Partner Ecosystem, as part of the elite “SellWith8” tier. This partnership integrates Regal.io’s advanced outbound dialing capabilities with 8x8’s contact center and UC platform, enhancing outbound communications (voice calls and SMS) for sales and support teams. By combining Regal.io’s proactive outreach tools with 8x8’s omnichannel contact center, customers can improve connect rates and customer engagement, all within a unified platform.

Microsoft Teams Integration: Alongside the above, 8x8 expanded its integrations with third-party collaboration tools. The company rolled out 8x8 Operator Connect for Microsoft Teams, enabling Teams users to natively use 8x8’s telephony (PSTN calling) on the Teams interface. 8x8 now offers a full suite of UCaaS solutions for organizations using Microsoft Teams, plus one of the few Teams-certified native contact center integrations. This helped win customers like Atrio Health, which leverage 8x8’s voice integration for Teams together with 8x8’s contact center.

Industry Recognition: The innovation and execution in Q1 earned 8x8 a few industry accolades. The company won two 2024 ChannelVision Visionary Spotlight Awards – one for Business Technology (8x8 Contact Center) and one for Overall Excellence for the 8x8 Elevate partner program. Additionally, TrustRadius recognized 8x8 as a leader in both the UCaaS and Contact Center software categories based on user reviews. Such awards bolster 8x8’s credibility in a competitive market.

Overall, 8x8’s product development in the quarter centered on AI-driven enhancements and expanding omnichannel capabilities, reinforcing the value proposition of its single-platform XCaaS solution. These updates aim to keep existing customers engaged (by delivering more value/features) and to make 8x8’s offering more compelling versus competitors’ point solutions.

Executive & Earnings Call Commentary

On the earnings call and in the Q1 report, management struck a balanced tone – highlighting operational successes (innovation, debt reduction) while acknowledging growth challenges.

CEO’s Perspective: CEO Samuel Wilson expressed satisfaction that 8x8 delivered “solid results” within guidance for the quarter. He emphasized that the company’s “ongoing innovation and strategic focus” are paying off in the form of continued adoption of 8x8’s modern customer experience (CX) platform. In particular, Wilson noted 8x8 is seeing “accelerated adoption of our solutions to address digital and more complex use cases” and growth in the number of contact center agents, especially in enterprise customers. This underscores 8x8’s strategy to deepen penetration in larger accounts with its XCaaS suite. Wilson reiterated that 8x8 remains focused on leveraging its platform to “deliver superior outcomes for our customers and stakeholders” – a nod to both customer success and shareholder value. In practical terms, this means balancing growth initiatives with profitability. Importantly, management’s commentary suggested confidence that as headwinds from legacy product churn abate (e.g. Fuze transition), organic growth will resume driven by cloud contact center and CPaaS momentum.

CFO’s Perspective & Debt Reduction: CFO Kevin Kraus highlighted a major financial milestone achieved just after the quarter – the early repayment of 8x8’s term loan from Francisco Partners. In early Q2 (July 2024), 8x8 secured a new $200 million bank term loan facility and on August 5, 2024 used those funds plus ~$29 million in cash to fully pay off the remaining $225 million on the higher-interest term loan. Kraus noted this move reduced the company’s debt substantially: since August 2022, 8x8 cut total principal debt (including convertibles) by $146 million (27%), strengthening the balance sheet. He stated this debt reduction aligns with 8x8’s objective to return value to shareholders and improve financial flexibility. The refinancing at a favorable interest rate with reputable banks was also cited as a vote of confidence by lenders in 8x8’s path to sustained profitability and cash flow generation. From an operational standpoint, lower debt and interest expense should help 8x8 maintain its margin targets even if revenue growth is modest in the near term.

Other Commentary: Management indicated that the company is prioritizing profitability and cash flow amid the lower growth environment. R&D investment remains high (to drive the AI and platform advancements discussed), but 8x8 also undertook cost optimizations in areas like general and administrative expenses. They expressed confidence in hitting the non-GAAP operating margin guide of ~10% for FY25. The team also discussed shifting business metrics – with more usage-based revenue, they’re focusing on new KPIs (like perhaps net dollar retention or usage growth) since ARR will be de-emphasized.

Overall, the executive tone was cautiously optimistic: acknowledging that the market environment and macroeconomic backdrop were challenging, but pointing to leading indicators of improvement (enterprise CCaaS uptake, successful product launches, debt improvement) that lay a foundation for returning to growth.

Market Reaction and Analyst Insights

Investors and analysts reacted to 8x8’s Q1 FY2025 earnings with a mix of caution and mild encouragement. The results were largely in line with expectations, but the lack of growth gave some pause. Key observations include:

Stock Performance: Following the earnings release on August 7, 2024, 8x8’s stock declined in the immediate aftermath. The day after the report, EGHT shares fell roughly 5–8% and traded in the high-$2 range (around $2.69 by close of Aug 8) as the market digested the flat revenue outlook and continued year-over-year decline. This drop erased a small rally the stock had prior to earnings. In the bigger picture, 8x8’s share price had been on a downward trajectory through 2024, reflecting investor concerns about its growth prospects. By mid-2025, EGHT was down over 50% year-to-date and hovering under $2, significantly below its 52-week high of $4.21 in August 2023. The muted reaction to Q1 FY25 results signaled that investors wanted to see a clear return to growth before getting more bullish on the stock.

Analyst Commentary: Financial analysts viewed the quarter as uninspiring but not alarming. The 1–3% revenue decline was anticipated, and both revenue and EPS came in essentially at consensus estimates. Non-GAAP EPS of $0.08 matched expectations and showed that 8x8 can sustain profitability at the current scale. However, analysts noted that 8x8’s growth lags the broader UCaaS/CCaaS industry. Some commentary pointed out that “8x8 reported a rather uninspiring 1.3% year-on-year revenue decline… in line with Wall Street’s estimates”, and that management’s FY2026 revenue outlook (given during later updates) implied only a slight improvement to flat growth. In other words, the turnaround to solid growth was not yet evident, tempering enthusiasm. On the positive side, analysts acknowledged the improving operating margins and cash flow. They also saw the contact center traction and AI feature rollout as potential tailwinds for re-accelerating growth in coming quarters – but execution will be key.

Stock Consensus: As of Q1 FY25, the analyst consensus rating on 8x8 was mixed, leaning cautious. Many analysts had a Hold or Underperform rating on EGHT. The average 12-month price target was around $2.50–$3.00, not far from the trading price at the time (implying modest upside). This reflected a wait-and-see approach: analysts want to see evidence that 8x8 can hit its flat revenue guidance (or beat it) and resume growth in the UCaaS/CCaaS market before recommending the stock more strongly.

In summary, the market’s reaction to 8x8’s Q1 FY25 earnings was reserved. The company’s stable margins and product improvements were acknowledged, but the declining top line and soft near-term outlook kept investors on the sidelines.

Competitive Landscape Comparison

8x8 operates in the highly competitive cloud communications arena, going up against both pure-play UC/CC providers and tech giants. A look at competitors’ performance during a similar timeframe provides context for 8x8’s results:

RingCentral: A leading UCaaS competitor, RingCentral reported 10% year-over-year revenue growth to $593 million in the quarter ending June 30, 2024 – a stark contrast to 8x8’s revenue decline. RingCentral’s higher growth was driven by its large enterprise UCaaS base and partnerships (RingCentral provides UCaaS while leveraging integrations with contact center partners like NICE inContact). Even though RingCentral’s growth had slowed in recent years, by mid-2024 it was still managing high-single to low-double-digit expansion, and it raised its full-year subscription revenue guidance to ~9% growth. RingCentral’s scale (quarterly revenue ~$600M vs 8x8’s ~$178M) and brand presence make it a formidable competitor. 8x8 is trying to differentiate by offering a single-platform XCaaS (whereas RingCentral often sells UCaaS and relies on third parties for CCaaS), but RingCentral’s sales reach and larger installed base give it an advantage in pure UCaaS deals.

Five9: In the pure-play CCaaS segment, Five9 Inc. is a key competitor focusing on cloud contact centers. Five9’s growth outpaced 8x8 – for the quarter coinciding with 8x8’s Q1 FY25, Five9 posted 13% revenue growth (reaching $252.1 million for Q2 2024, up from $222.9M a year prior). Five9 highlighted particularly strong enterprise subscription gains (over 20% growth in large-client subscription revenue) and surpassed a $1 billion annual revenue run-rate during 2024. The company’s focus on contact center software and AI (Five9 has its own IVA – intelligent virtual assistant – offerings and is investing in automation) directly overlaps with 8x8’s CCaaS business. Five9’s solid double-digit growth underscores that the cloud contact center market remains in expansion mode, even as 8x8’s total revenue was flat/down – suggesting 8x8 has room to capture more of that growth if it can execute in sales and product differentiation.

Other Peers: Zoom has entered the space (offering Zoom Phone for UCaaS and leveraging partners for contact center), and while Zoom’s overall growth slowed in 2024, its Zoom Phone product was growing strongly ( Zoom Phone reached 10–20% YoY growth rates, albeit from a smaller base). Microsoft and Cisco (Webex) present competition by bundling voice/meeting solutions with broader enterprise software suites. Meanwhile, NICE CXone (by NICE Ltd.) and Genesys remain leaders in cloud contact center for large enterprises. For instance, NICE reported accelerating cloud revenue in early 2025 as customers migrated from legacy on-premise systems. These larger competitors often appear in deals 8x8 chases, especially on the contact center side.

Compared to these peers, 8x8’s growth underperformance in Q1 FY25 was evident. Both major UCaaS and CCaaS rivals were still growing their top lines in the mid to high single digits (or more) versus 8x8’s slight decline. However, 8x8’s strategy of integrating UCaaS and CCaaS is somewhat unique among smaller players, potentially appealing to mid-market customers who want one vendor for all communications. The challenge will be for 8x8 to reignite growth by capitalizing on its recent AI innovations and cross-selling its platform to more enterprises, while fending off rivals.

On a positive note, 8x8’s focus on AI and workflow automation is in step with industry trends – competitors like RingCentral and Five9 are also touting AI features, so 8x8 must continue to innovate to stay relevant. The company’s recognition by TrustRadius as a leader in both UCaaS and CCaaS categories indicates it has a competitive product; translating that into improved sales and marketing execution will be key. As the UCaaS/CCaaS market evolves (with convergence of communication APIs, contact center, and collaboration), 8x8’s ability to deliver an end-to-end solution could become a stronger differentiator if it demonstrates tangible customer ROI (as seen in the case studies like Oldham Council’s savings and Atrio Health’s compliance win).

In summary, 8x8’s Q1 FY2025 earnings showed a company in transition – holding margins and innovating aggressively with AI, but working through legacy churn and flat revenue. The quarter’s solid operational execution (meeting guidance, cutting debt, launching new products) was a promising sign, yet investors remain focused on when growth will return. Going forward, success for 8x8 will be measured by its ability to convert product innovation and enterprise wins into sustained revenue growth, closing the gap with faster-growing competitors in the UCaaS/CCaaS space. The foundations laid in Q1 FY25 – from AI features to high-profile customer deployments – are intended to drive that next phase of growth in the coming quarters.

8x8 Q1 FY2025 Earnings: Frequently Asked Questions

What were 8x8's key financial results for Q1 FY2025?

In the first quarter of fiscal year 2025 (ended June 30, 2024), 8x8 reported total revenue of $178.1 million, a decrease from $183.3 million in the same period last year. Service revenue, which is recurring subscriptions, was $172.8 million, also down from $175.2 million a year ago. While revenue saw a year-over-year decline of approximately 2.8%, it was largely stable sequentially compared to Q4 FY2024 ($179.4 million). The GAAP net loss improved significantly, narrowing to $10.3 million from a $15.3 million loss in the prior year, thanks to cost controls and debt refinancing benefits. On a non-GAAP basis, the company remained profitable with net income of $10.4 million. Adjusted EBITDA was $25.8 million, and the non-GAAP operating margin was around 11%, within the company's guidance range.

Why did 8x8's revenue decline year-over-year in Q1 FY2025?

The year-over-year revenue decline was primarily attributed to the ongoing runoff of legacy revenues from the acquisition of Fuze in 2022. Many former Fuze customers had not yet migrated to 8x8's platform, resulting in customer churn and revenue attrition. Management noted that if the decline from these former Fuze platform customers were excluded, core service revenue would have grown nearly 5% year-over-year.

What is 8x8's near-term revenue outlook and growth strategy?

8x8's guidance for Q2 FY2025 projects total revenue between $175 million and $181 million, implying a flat-to-slightly down trajectory year-over-year. For the full fiscal year 2025, the company forecasts total revenue of $710 million to $732 million, which would represent approximately 0% to +0.5% growth over FY2024's $729 million. This cautious outlook reflects the challenges of transitioning its customer base and product mix, specifically addressing the remaining Fuze legacy churn. The growth strategy is centered on the integrated XCaaS platform (combining UCaaS and CCaaS), with a strong emphasis on accelerating adoption of their Contact Center (CCaaS) solutions, particularly in enterprise customer deployments, and leveraging new AI-powered capabilities and product launches to drive customer value and upsell opportunities.

How is 8x8 addressing the churn from the acquired Fuze customer base?

8x8 is actively working to migrate the remaining former Fuze customers to its modern 8x8 XCaaS platform. The company expects to complete all these migrations by the end of calendar year 2025. While this migration process is currently contributing to year-over-year revenue headwinds, its completion is anticipated to reduce this source of churn and help stabilize and grow recurring revenues going forward.

What key product innovations and features did 8x8 highlight in Q1 FY2025?

8x8 highlighted significant product development, focusing heavily on integrating AI across its platform. Key innovations included deploying a more powerful large language model for improved speech transcription and language support in interaction analytics, introducing AI-based interaction summaries that integrate with CRM systems, and offering a "bring-your-own-AI" capability for contact centers. New solutions launched include 8x8 Ballot It! (an AI-powered self-service tool for UK local governments), 8x8 Intelligent Customer Assistant - Voice (adding voice support to their conversational AI bot), and Interact for Proactive Outreach (an omnichannel outbound messaging tool for SMS and WhatsApp). The company also expanded its integrations, notably with the launch of 8x8 Operator Connect for Microsoft Teams.

What is the strategic importance of the Contact Center (CCaaS) segment for 8x8?

The Contact Center-as-a-Service (CCaaS) segment is strategically crucial for 8x8 and is showing strong momentum. Management noted accelerated growth in the number of contact center agents, especially among enterprise customers, driven by continued adoption of their modern CX platform. This growth in contact center users helps offset churn in legacy products. 8x8's strategy of selling integrated UCaaS+CCaaS deals (XCaaS) to larger enterprises is leading to larger contact center deployments and higher-value subscriptions, as demonstrated by customer wins with Great Places Housing Group and ATRIO Health Plans which selected 8x8 specifically for its combined platform capabilities and advanced features like compliance and AI.

How did 8x8 address its debt position?

Just after the close of Q1 FY2025, in early Q2 FY2025 (specifically on August 5, 2024), 8x8 successfully paid off the remaining $225 million on its term loan from Francisco Partners. The company secured a new $200 million bank term loan facility and used those funds along with approximately $29 million in cash for the early repayment. This move substantially reduced 8x8's total principal debt by $146 million (27%) since August 2022, strengthening the balance sheet and improving financial flexibility at a favorable interest rate.

How did the market and analysts react to 8x8's Q1 FY2025 results?

The market reaction to 8x8's Q1 FY2025 earnings was reserved and cautious. Following the earnings release, the stock declined, reflecting investor concerns about the flat revenue outlook and continued year-over-year decline. Analysts viewed the quarter as uninspiring but not alarming, with results generally in line with estimates. While acknowledging the improving margins, cash flow, contact center traction, and AI feature rollout as potential future tailwinds, analysts noted that 8x8's growth is lagging behind the broader UCaaS/CCaaS industry, with competitors like RingCentral and Five9 reporting solid growth. The analyst consensus remained mixed, leaning cautious, with a wait-and-see approach pending clear evidence of a return to sustained revenue growth.

Sources:

8x8, Inc. Q1 FY2025 Financial Results Press Release

8x8 Q1 FY25 Earnings Call/CEO Blog Highlights

StockStory / Analyst commentary on 8x8’s earnings and outlook

Competitor earnings releases: RingCentral Q2 2024; Five9 Q2 2024.